Peachy Green

An Overview of Georgia’s Medical Cannabis Roll-Out

The Southern Charm of Georgia Cannabis

Georgia’s medical cannabis rollout has been marred with delays, lawsuits, and last minute changes that are becoming typical to any of the developing cannabis program in the United States. With the likes of Cannabis companies Curaleaf, Trulieve, Parallel, Verano & Columbia Care all applying for a license in Georgia. To be one of the 6 lucky winners out of 69 applicants in Georgia, required an incredible amount of capital, lobbying, and groundwork over the past three years - at a minimum.

At first glance, the main attractions for being in Georgia is that the state has one of the fastest-growing populations in the US. Most notably, Georgia is home to Atlanta, which is home to about ~500k people and a cultural cornerstone of the south. While the state of Georgia as a whole is called home for ~11m Americans. The proportion of Georgia’s population that is 60 and older is growing more rapidly than other components of the population. Making Georgia a very suitable state for a medical marijuana program to thrive. Very similar to that of Florida.

However, not everything is peachy keen in Georgia when it comes to it’s Medical Cannabis program. Georgia's Access to Medical Cannabis Commission has a very narrow scope of permissible medical ailments, limited products and low THC % limits that could hamper long term growth. But overall, the benefits of operating here are considered not to be limited to the state’s program or borders. As other southeastern states yet to legalize cannabis will be heavily influenced by Georgia’s program and those successful operators.

Georgia’s Regulatory Framework

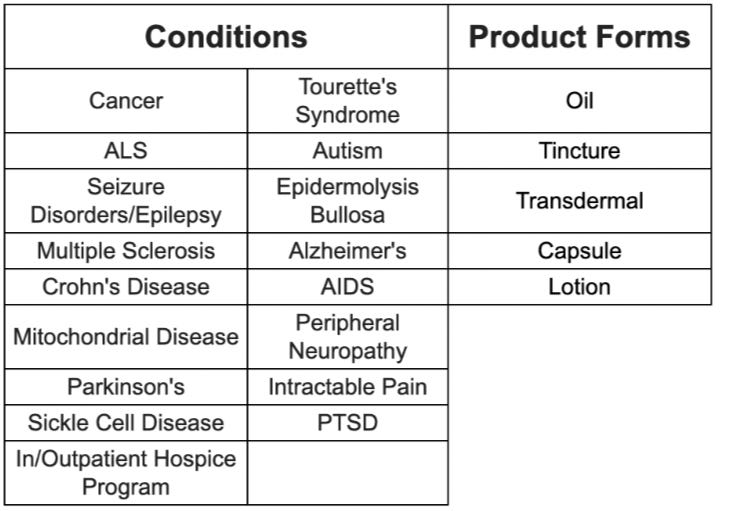

In short, Georgia’s regulatory framework heavily mirrors Florida, by far the most favorable market to hold a license in. The initial medical legalization legislation passed in April 2019, HB 324, laid out a framework for low-THC cannabis to be produced and dispensed by: (2) Class 1 licensees who have a limit of 100,000 square feet of cultivation space, and (4) Class 2 licensees who have a limit of 50,000 square feet. It also established a list of 17 qualifying conditions for patients, and 5 allowable product forms with an initial 5% THC limit (see below). The Georgia Access to Medical Cannabis Commission was also formed, which will oversee the medical program and conducted this first licensing round.

An expansion law passed in May 2021, SB 195, provided a framework for bona fide partnerships between licensees and universities, and a few expanded rights for licensees. For instance, each licensee will initially be allowed 5 dispensary locations. When the patient count hits 25,000, and for every 15,000 patient increase thereafter, each licensee will be issued an additional location.

Georgia’s Winners & Losers

Class 1 License Winners:

Score: 933.75

While not many people were surprised at Trulieve’s success here, this is a highly significant win for them. Their production facility will be located in Adel, a mere 40 minutes from the Florida border. As one common critique of MSOs is the lack of consistent operating practices between facilities, having the ability to have experienced team members from your largest market oversee the buildout, operations, and troubleshoot on short notice is invaluable.

Score: 970

Botanical Sciences is primarily a local group run by Robin Fowler MD, the owner of a pain management center in Georgia. Their operating partner will be Altitude, a vertically integrated dispensary chain in Colorado. Botanical Sciences will be building out in Glennville, in the southeastern region of the state.

Class 2 License Winners:

Natures GA LLC, DBA Nature’s Medicines

Score: 876.25

Nature’s Medicines is a private MSO with operations in 6 states: Pennsylvania, Missouri, Arizona, Maryland, Massachusetts, and Michigan. Winning limited licenses has long been one of their strengths. They will center operations in Dublin, a small city in central Georgia.

Score: 870

Treevana Remedy is a group that’s backed by Whole Plants, a Pennsylvania Grower-Processor, and Stem Holdings. Stem currently owns 2.5%, will be increasing that equity stake, and will be an operating partner. Treevana will be building its facility near the campus of Central State Hospital in Milledgeville, which is the state’s largest facility for treating mental illness and developmental disabilities.

Score: 888.75

Starting in 2020, TheraTrue has been making the media rounds as an upstart, minority-owned cannabis business with Victor E. Mancebo, former CEO of Liberty Health Sciences at the helm. They’ve also applied for the HSA1 region license in Virginia, to take Pharmacann/Medmen’s revoked spot. They will be operating in Louisville, an eastern city that was formerly the capital of Georgia. They are also GTI’s Georgia partner, and likely their partner in Virginia.

FFD GA Holdings LLC, DBA Fine Fettle

Score: 893.75

Fine Fettle is a northeastern-focused MSO with operations in Connecticut and Massachusetts, with additional expansion plans in the works. They are primarily self-backed and will be establishing operations in Macon, a small city in the central part of the state.

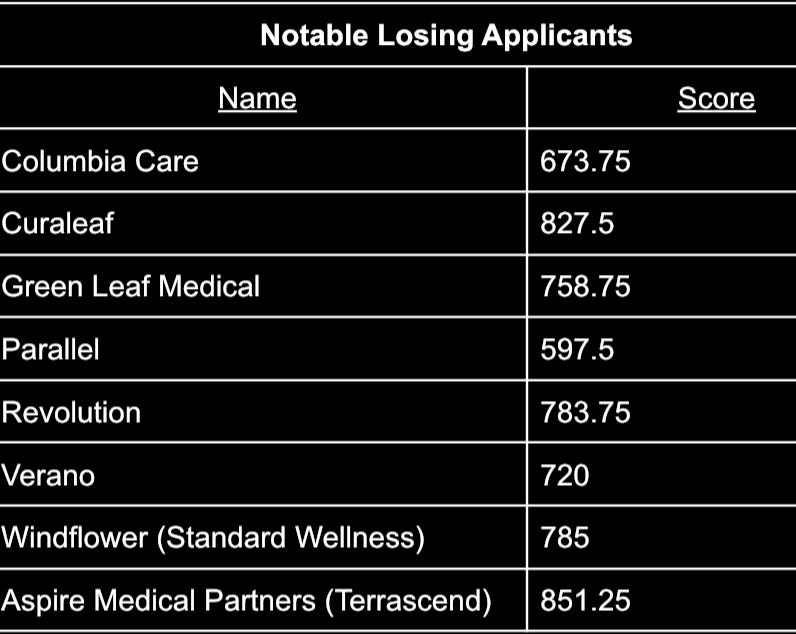

Notable Losing Applicants

Of all the companies that lost out (see table below), the most surprising is Parallel. They’ve long had their corporate headquarters in Atlanta and have spent a lot of money on lobbying. Many investors saw them winning in Georgia almost as a given. However, of all the publicly listed companies they scored the LP’s west score of the bunch. Then, Acreage Holdings who was considered the front runner 2 years ago with it’s partner’s Compass & Forsyth County - didn’t even apply. Then, with Jason Wild being the Chairman of the Board of TerrAscend Corp. and Georgia based Arbor Pharmaceuticals. TerrAscend investors had high hopes that their partner Aspire would have won but they didn’t make the cut. You can see the Class 1 scores here and the Class 2 scores here.

However there remains to be hope for some of the losers. Moments before announcing the license winners, the Georgia Commission did say they will be recommending the issuance of 2-4 additional licenses. If they pick those additional companies from this recent licensing round, below is a table displaying the next-highest scoring companies. As one can imagine, there’s already been 7 Class 1 license protests and 14 Class 2 license protests filed by losing companies - this strategy has worked in similar limited license markets before.

Kim Rivers & Trulieve’s Southern Charm

Being the only publicly traded MSO to directly win in Georgia has not only strengthened Trulieve’s stranglehold on the southeast, but shows they can prudently expand without sacrificing significant amounts of equity for partnerships or capital to purchase already issued licenses. The likes of Boris Jordan and Curaleaf are probably scratching their heads wondering how did Kim & Trulieve accomplish this?

Trulieve started to lay it’s groundwork in Georgia early and forcefully. They overpowered their opponents in key areas in achieving the highest point score of all those applied. Achieving a 106.25 higher positive point differential than that of Curaleaf. This didn’t happen by chance. Numerous strategic events leading up to the latest announcement insured Trulieve would not just win but dominate.

For instance, Trulieve contracted the highest number of lobbyists in Georgia as a public MSO (11), with Curaleaf coming in second with 5. Trulieve hired the state House Speaker David Ralston son, Matthew Ralston, as one of its lobbyists. While it’s also been said that Trulieve’s main Florida lobbyist group in Ballard Partners. Has built a reputation for having far reaching influence stretching to many parts of the southern US including that of Georgia.

When things didn’t seem like they were going in Trulieve’s favour in Georgia. Just a few days before the application deadline. Not only did they file a protest with the regulators. They sued the state challenging the requirement that applying entities must have operated in GA for a minimum of 5 years. Giving Trulieve the necessary time to submit a robust Request for Proposal and ultimately change their subsidiary in Georgia from one formed in 2019 to one formed in 1993. Only to withdraw the protest and lawsuit almost a month after filing.

While Trulieve has been dismissed by other MSO’s as simply being a Single-State-Operator. Achieving first mover advantage has always been their preferential strategy for entering a limited license state. This is strategy in Florida and this is the strategy they are looking to employ in every emerging market - for instance, they already have entities established in preparation for application rounds in Alabama, Mississippi, Texas, Virginia, and New Jersey.

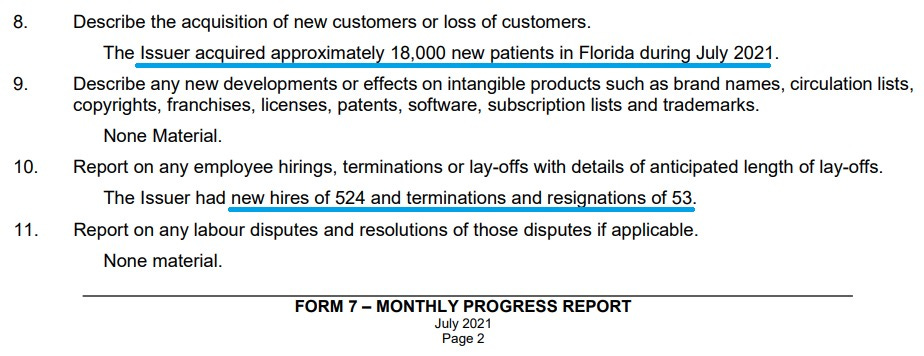

The rules in Georgia that for every 15,000 patient increase thereafter the first 25,000 the company is permitted open one storefront in addition to the initial 5. Seems almost tailor made for Kim Rivers to thrive. With Trulieve onboarding 18,000 patients in Florida during July (see above). Trulieve has increased it’s patient count in Florida with ease. If Trulieve can emulate that success in Georgia. Bless her heart, Kim River’s is about to become Georgia's version of Princess Peach.

Now that the smoke has cleared surrounding the license applications. There remains to be three elephants in the room: The 5% THC limit on all products, no availability of smokable flower/edibles and the limited number of conditions. However our thought process remains steadfast that Georgia will follow the lead of Florida. If you recall the initial legalization efforts in Florida. The THC limit was originally just 0.8% THC & 10% CBD with the conditions limited to patients with cancer or a “physical medical condition that chronically produces symptoms of seizures or severe and persistent muscle spasms” may qualify for the program if no satisfactory alternative treatment options exist.

As one can imagine, the regulators of respective state medical cannabis programs talk to one another to gain insight and lessons learned. When early movers such as Florida implemented low-THC programs, their program administrators had little to draw upon other than west coast markets that were highly volatile and mostly not politically congruent. Now that Georgia’s Commission has mature highly regulated medical markets such as Florida, Pennsylvania, Ohio, and Connecticut to draw years of wisdom from, there is reason to believe their market’s development will be accelerated compared to the aforementioned.

Additionally, the Georgia Commission’s independent work will only be compounded by the work of licensees. If you want to get additional qualifying conditions such as anxiety added to a program, you need to prove the merits of cannabis treatment to the Commission. This is why partnering with medical institutions is just as important for winning a license as it is for operating. Public-private partnerships such as Trulieve’s partnership with the Morehouse School of Medicine, and Botanical Science’s partnership with Georgia Southern will prove incredibly useful to prove the efficacy of medical cannabis to regulators.

While the same formidable issues in Georgia still linger in Florida. They’ve all been handedly defeated. “I have not endorsed (capping THC),” said Gov DeSantis in regards to an attempt to cap THC. Edibles have been introduced in Florida in 2021. While patients certified or recertified to smoke medical marijuana in Florida must sign a new standardized consent form in 2021. However, the best weapon for enacting progressive change is by stating the alternative: The Black Market.

While the near term goal in Florida is that of full recreational legalization. The black market up against a limited medical marijuana program will be formidable as it’s always been in the south. To the contrary of Georgia & Florida there is a lot of negative commentary on Oklahoma prematurely trying to become the leader in interstate commerce. Something Georgia regulators are desperately trying to avoid.

Overall, the short-medium term benefits of operating in Georgia are obvious: a highly restricted market with a large population, in the region that’s the final frontier of US cannabis legalization. In the long-term, the state’s microclimate and low environmental risk offer the opportunity to establish production facilities that can supply much of the southeast and greater east coast.